Eutelsat is held together by politics, not performance.

History

Eutelsat Communications S.A. (European Telecommunications Satellite Organization) is a Paris-based company providing communication solutions via its own satellite infrastructure. The company currently operates 35 geostationary (GEO) satellites and, by its own account, approximately 600 low-Earth orbit (LEO) satellites. With a market capitalization at around EUR 2 billion, this makes it the world’s third-largest satellite operator.

Eutelsat’s business is divided into two main segments: Video (primarily satellite TV broadcast via GEO satellites) and Connectivity (internet access via LEO satellites). In its segment reporting, Connectivity is further broken down into mobile internet (ships, aircraft), fixed internet (homes, offices), and government services.

The company’s roots lie in a pan-European intergovernmental organization founded in 1982 through a treaty between 26 European countries. Its original mandate was to commercialize communication satellites developed by the European Space Agency (ESA).

Eutelsat was privatized in 2001. However, the years that followed were marked by disputes with former state stakeholders, particularly due to service disruptions and quality issues. The first IPO attempt in October 2005 was cancelled amid investor concerns over an overly ambitious price range and a lack of trust in management, with fears that executives would sell their shares immediately after listing. The IPO eventually took place two months later in December 2005, but at a reduced price of EUR 12 (down from an intended EUR 15.50–17.55). Part of the deal were strict conditions imposed on how and when management could sell shares.

Until 2023, Eutelsat’s core business involved broadcasting around 5,500 TV channels to roughly 200 million receivers across Europe, the Middle East, and Africa. The acquisition of British company OneWeb in September 2023 marked the company’s expansion into global internet provision via LEO satellites.

The ownership structure reflects the company’s close ties to the state. Behind Bharti Global (24%) (the investment arm of Indian conglomerate Bharti Enterprises and former majority owner of OneWeb), the largest shareholders are the governments of France (16%) and the UK (11%).

Management

In May 2025, Eutelsat announced that CEO Eva Berneke would be replaced by Jean-François Fallacher. This followed a board reshuffle in February that led to the resignation of five directors (Mia Brunell, Esther Gaide, Cynthia Gordon, Fleur Pellerin, and Dominique D’Hinnin).

Berneke oversaw the merger and integration of OneWeb, but her actions reportedly infuriated then-EU Commissioner Thierry Breton, who viewed the move as a betrayal of his European industrial vision for Eutelsat. Breton, often described as the “Commissioner of Corporations”, had different ambitions for the company.

Now, Jean-François Fallacher, who is a former executive at France Telecom and who worked under Breton during his tenure, steps into the role. Classic EU-style cronyism.

While Eutelsat’s strategic future lies in technology and services acquired via OneWeb, the appointment of Fallacher signals tightening control by the French republic. This raises concerns over cultural and operational friction, as a French-controlled headquarter may not be the best corporate culture match to lead an innovative UK-based technology business.

Controversies

France’s role has also been controversial when it comes to sanctions’ enforcement. Despite clear breaches of EU sanctions against Russia, Eutelsat continues to broadcast channels linked to the Russian military and private Russian networks. Another example is the Al Aqsa channel, which is associated with Hamas.

Eutelsat stated that these accounts represent about 4% of total revenue. However, the company claims that they cannot afford this kind of loss. French parliament had to appeal twice to the national broadcasting regulator to force Eutelsat to stop airing these channels. Despite being the largest public shareholder, the French government refused to apply pressure. While usually eager to take action against Russia, this time hypocrisy and business interests seem to have prevailed.

Hype

After trading for a long time between EUR 1 and 2, Eutelsat’s stock suddenly surged to over EUR 8 in March 2025. The driver appears to have been the French government’s suggestion that Eutelsat could become Europe’s answer to Starlink.

Amid the current geopolitical shift, Europe’s involvement in the Ukraine conflict, and the general mistrust of a potential second Trump administration by many left-leaning EU governments (including the EU Commission itself), European leaders were resistant to further rely on Elon Musk’s Starlink for satellite infrastructure. For a short moment, Eutelsat seemed to offer an European solution – a platform that could play a central role in a future EU military satellite network.

Investors hoped for strong public support, especially given the company’s politically connected shareholders. But optimism didn’t last long. The gap with Starlink turned out to be much wider than expected, required subsidies much larger, and the EU’s willingness to actually invest in Eutelsat much lower than anticipated.

Now, even with public subsidies, Eutelsat faces massive financial uncertainty.

Competition

Although Eutelsat is framed as an European alternative to Starlink, Starlink is way ahead on nearly every front. While Eutelsat doesn’t disclose pricing, Reuters reports that Starlink terminals cost around EUR 500, whereas Eutelsat’s solutions are 10 to 20 times more expensive. Service subscriptions from Starlink are also significantly cheaper.

A quick comparison shows the diverging dimensions by which Eutelsat is falling behind: Starlink operates over 7,000 LEO satellites. Eutelsat? Only around 600.

Right now, Eutelsat’s only unique selling point is that it’s not Starlink. We doubt this will be enough to sustain.

And we haven’t even talked about Amazon’s Project Kuiper as additional competition for LEO satellites. Although services haven’t launched yet, Kuiper already has 4,000 satellites in orbit.

Nonetheless, Eutelsat will most probably survive thanks to EU and government funding. Although it is obvious to everyone that it’s just another inferior and overpriced European copy of a working American model, tax income of the European debt union will safe them all – again.

Financials

Fact is, the group’s recent financial performance has been disappointing. Latest publications show that losses have deepened, and net debt has ballooned to EUR 3.0 billion mid 2025. Those numbers are clearly unsustainable.

In March 2025, Fitch downgraded Eutelsat’s credit rating, citing slow revenue growth at OneWeb and heavy capital requirements for maintaining the LEO satellite fleet. In addition, the company faces major refinancing obligations in 2026 and 2027.

Goldman Sachs rates Eutelsat a Sell, with a price target of EUR 1 (yes, ONE). Other analysts have also raised concerns given potentially overestimated expectations regarding OneWeb.

A closer look at the 2025 half-year report shows that goodwill made up more than 18% of non-current assets, or 15% of the total balance sheet at the beginning of the year. For the half-year, Eutelsat reported an impairment of EUR 535 million in goodwill, against half-year revenues of only EUR 606 million. To write down over half a billion euros in goodwill in just six months raises serious questions: Were these acquisitions overpriced from the start?

Because of this adjustment, operating income fell to a loss of EUR 790 million, compared to a profit of EUR 134 million in H1 2024. Even if you exclude goodwill impairment, H1 2025 still saw a loss of EUR 255 million, which almost doubles the loss from the previous year.

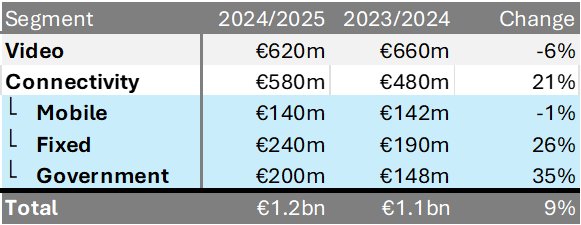

The following table shows Eutelsat’s revenues broken down by segments.

While the Video segment is Eutelsat’s traditional business, Connectivity includes the services acquired with OneWeb. The size and growth of the Government segment is particularly striking. It shows that Eutelsat not only relies on the state as an owner and lender of last resort, but also as a key customer, generating nearly 20% of total revenue.

That may provide some stability, but socialism has shown that state-dependent companies rarely thrive in the long run. Eutelsat is another example to that story.

And just as we were finishing this report, news broke that France plans to inject another EUR 1.5 billion into Eutelsat through a capital increase.

Conclusion

In our view, Eutelsat lags far behind competitors like Starlink and Kuiper in terms of technology, scale, and innovation. Its only real selling point is that it’s not American – which may excite some European politicians but doesn’t attract commercial or private customers that are faced with uncompetitive prices and an outdated infrastructure.

Eutelsat is not a new short idea. But after the recent rally – driven by France’s capital injection and new CEO expectations, HitHawk believes the short case has regained its appeal just now.

At the current price of EUR 3.75 we believe Eutelsat is again significantly overvalued.

We adopt Goldman Sachs’ price target of EUR 1 as our own.

That is where Eutelsat seems fairly valued.