HitHawk is short Anbio Biotechnology (Nasdaq: NNNN).

Summary

The stock’s bizarre price behavior was the first red flag. A deeper investigation turned it into a full alarm: Anbio is not a misunderstood startup – more likely it is a purpose-built fraud machine.

From day one, the company’s architects laid the groundwork for a classic extraction scheme. The Cayman formation was not an accident; it was the launchpad. What followed reads like a fraud manual:

- Incorporate in a secrecy haven, funded with just $50k, to ensure opacity from the outset.

- Assemble a maze of shell companies, deliberately intertwined to hide flows of money and ownership.

- Explode the share count – turning 100 shares into 500 million while slashing par value from $500 to $0.0001.

- Dump massive blocks of near-worthless shares into the hands of untraceable recipients (143 million shares, 23 beneficiaries).

- Float the IPO at $5, not to raise capital, but to give a fictitious paper value a market sticker – roughly a 5,000,000% markup from par.

- Saturate the market with glossy narratives, ensuring there are always fresh buyers for the next extraction cycle.

- Crank up promotions before the IPO, including legally dubious stock touting.

- Harvest and repeat – pump, dump, convert paper into fiat, reset, and run the playbook again.

Let’s be blunt: Anbio is not a company.

It appears to have no products, no employees, no economic activity, and no legitimate corporate purpose. It looks more like a vessel designed to siphon money from public markets.

Investors should treat Anbio with the highest level of suspicion.

Don’t believe a word you hear.

We informed Nasdaq and the SEC about our findings.

Background

In September 2025, we received an anonymous tip regarding Anbio Biotechnology (Nasdaq: NNNN). After a quick review it became obvious that Anbio has no business model at all, but is an artificial shell created for one single purpose: to fraudulently extract money from investors. We posted a warning of a pump-and-dump scheme on September 10.

The share price development since the IPO is shown in the attached chart.

In June 2025, the stock was pushed up by 900% and peaked at $53.47 (August 19). Our warning tweet from September 10 came just in time. Shortly after, the downturn accelerated. By early November 2025, Anbio had lost 77% of its peak value ($12.29 on November 3).

However, the game started again. As of December 4, Anbio touched $42.99 (up again 250%).

This raised key questions for us: What exactly is behind this company? Did we overlook something? Are we witnessing a second run, a second full cycle of pump-and-dump? And where do all these new investors keep coming from?

Consequently, we looked at the company in more detail. And what we found is no good – and hard to believe.

Anbio Biotechnology

Anbio was founded in 2021 in the Cayman Islands. The founding capital was $50,000, divided into 100 shares. Suspiciously, no names of founders, directors, or CEOs could be identified.

The company claims to be an “innovative provider of biotechnology solutions”. However, Anbio’s records mainly show substantial efforts to create a murky network of additional entities – a common pattern for fraudulent companies. Wirecard, Benko, Greensill: all had opaque holding structures. It is always convenient to have plenty of ways to shift and hide funds behind untransparent businesses.

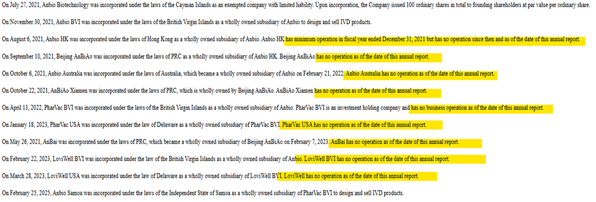

As of October 2025, the following subsidiaries form part of the network (Form 6-K, October 2025):

One should note the appealing offshore locations: British Virgin Islands, Samoa, Hong Kong, Australia, and the staggered founding years (2021-2025). However, none of these Anbio units have ever operated. They were established and then left idle, awaiting future use.

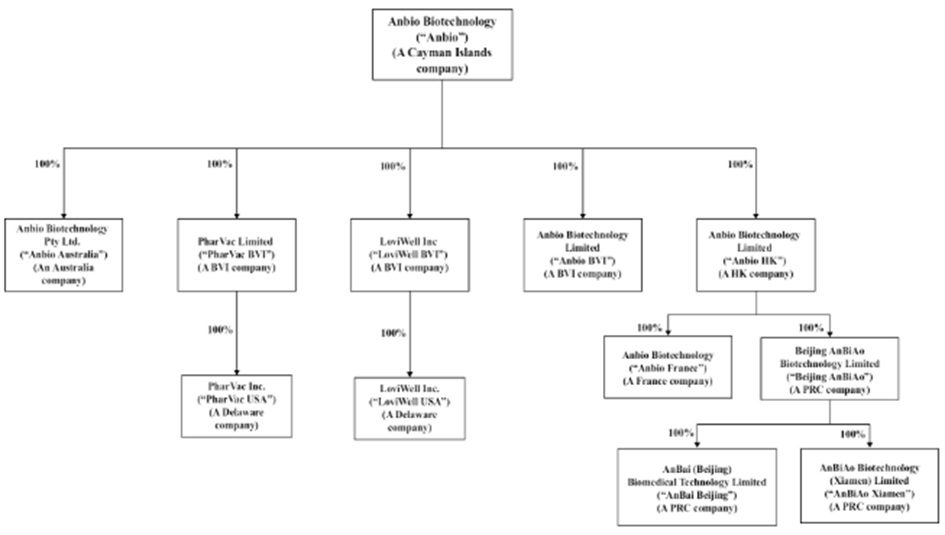

Ultimately, this has resulted in an impressive organizational chart of a supposed “global pharmaceutical group”:

Even if Anbio wanted to operate them, it could not. While Anbio claims to employ 27 people today, it declared zero employees for 2023 and 2024. In practice, Anbio has almost more subsidiaries than employees.

Restructuring before IPO

Parallel to the creation of new entities, a restructuring of the top-level ownership structure (Cayman-registered Anbio Biotechnology) was implemented on 30 June 2023, just before the IPO.

The 100 original shares (nominal value $500 each) were transformed into 500,000,000 shares with a par value of $0.0001. Of these, 80% (400 million shares) became Type A with one vote each. The remaining 100 million shares became Type B, granting 50 votes per share.

Go figure.

Paper Shells

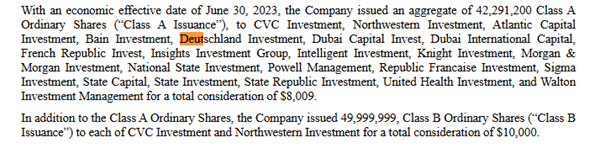

The next step was the allocation of ~143 million shares to “investment companies”. Among them: Atlantic Capital Invest, Bain Invest, Deutschland Invest, Dubai Capital Invest, etc. Names that are intentionally reminiscent of well-known firms, but that turn out not to be found anywhere nor being the big names as one would expect.

“Bain Investment”, for example, clearly wants readers to think of Bain Capital. They have nothing to do with each other.

Neither the “investment companies” nor their principals could be identified.

And the punchline: All 23 “investment firms” together invested $8,009.

Not millions. Not thousands each. Total: eight-thousand and nine dollars. Against a combined par value of ~$4,300. Those are classic paper shells.

It is obvious these shares were distributed to friends and associates who would benefit at the IPO. The IPO was priced at $5 per share. These shares suddenly had a paper value of ~$215 million.

By distributing stakes widely, they also cleverly avoided the 5% SEC regulation threshold, as every holder sits between 4.4% and 4.85%.

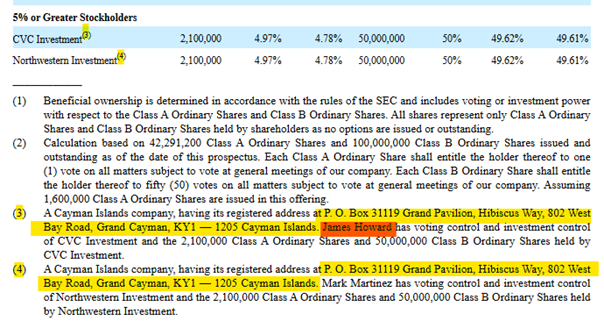

The Investors CVC and Northwestern

Two investors, CVC Investment and Northwestern Investment, play a special role.

Besides receiving Type A shares, they also each “purchased” 50 million Type B shares. All 100 million super-voting shares are held by these two entities. Each paid exactly $5,000.

This structure gives two partners gains far exceeding what the IPO proceeds could possibly justify. There was no economic reason to distribute these stakes before the IPO.

The SEC inquired about this. Anbio claimed the investors were expected to “help with access to customers”. Why CVC and Northwestern specifically – and not others – was not explained. Still, the SEC accepted the answer.

Remarkably, both investors are registered at the exact same mailbox address in the Caymans. Still, Anbio denied that they knew each other or acted in coordination. This becomes even more absurd when considering Anbio’s own Cayman mailbox address:

It remains unclear why the SEC, after accurately identifying key issues and inquiring about them, let Anbio pass – or whether it had to.

Mr. James Howard

As mentioned, responsible people are very hard to identify. For James Howard of CVC, our cross-check returned a match. All information are publicly available, and we believe, but cannot fully guarantee that it is the same individual running CVC-Investment. If it is, the result is explosive: James Howard was convicted in 2013 for a $21 million securities fraud.

From the U.S. Department of Justice:

“From approximately January 2010 through April 2011, Howard and his co-conspirators used material false and fraudulent representations and material omissions to obtain over $21 million from over 700 investors.” (https://www.justice.gov/usao-sdfl/pr/founder-investment-company-pleads-guilty-21-million-fraud-scheme)

The IPO Registration

Shortly after implementing the new capital structure, Anbio contacted Nasdaq and the SEC to register its shares for public trading.

At the outset, Anbio declared its Principal Executive Office to be:

Friedrich-Ebert-Anlage 49 (Messeturm), 60308 Frankfurt am Main, Germany.

The Messeturm is a prestigious landmark, but also known for virtual offices operated by Regus. The address is primarily used for mail forwarding and occasional meeting rooms. On-site verification confirmed that Anbio has no workspace, warehouse, administrative office, or laboratory at this location.

Anbio also never founded a German entity or registered a European office. No German legal entity forms part of Anbio’s corporate holdings.

However, things got worse: In October 2024, Anbio changed its address in SEC filings to:

Wilhelm-Gutbrod-Str. 21B, 60437 Frankfurt am Main, Germany.

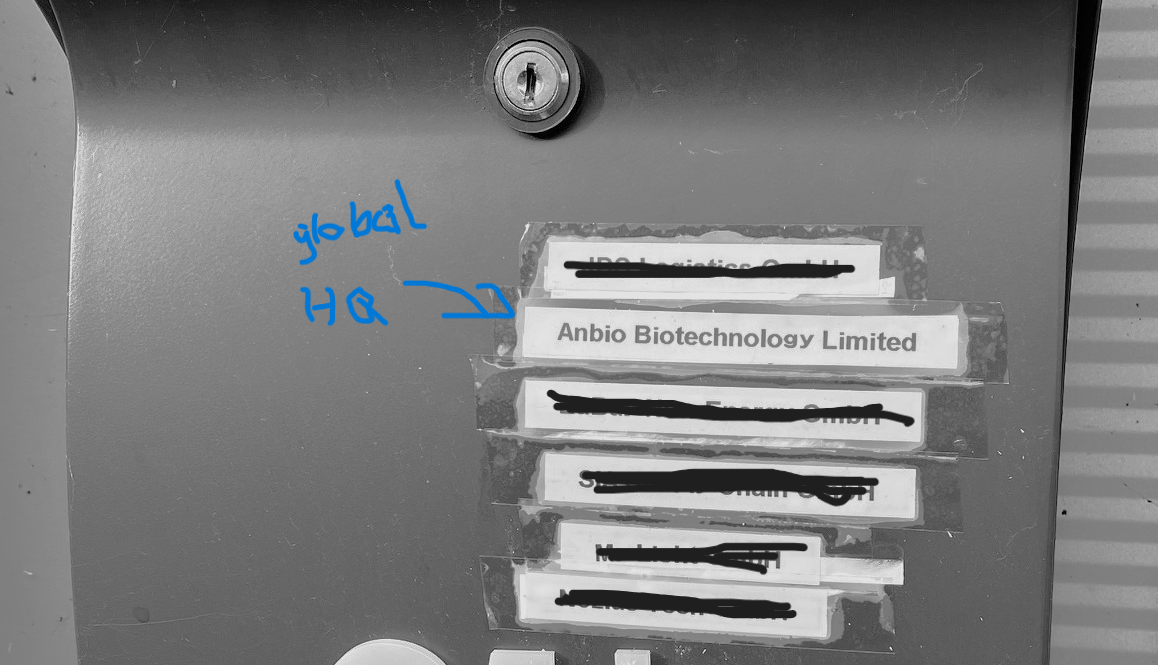

This address does not exist in municipal records. On-site verification we only found a mailbox label at a side entrance of an industrial building in the outskirts of Frankfurt. Anbio is one of six taped names on a shady mailbox. Clearly, we found the German headquarters, the principle executive office.

The surrounding area is a suburban industrial zone. No offices. No residential buildings. This raises serious concerns that the issuer is listing fictitious business locations.

Additionally, the telephone number provided to the SEC and Nasdaq is not a German landline but a prepaid mobile phone. This further contradicts Anbio’s claims of an established corporate presence.

You truly cannot make this up – and yet the facts get even more alarming.

Products

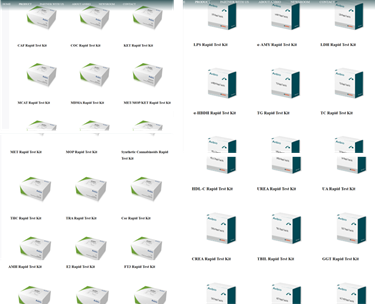

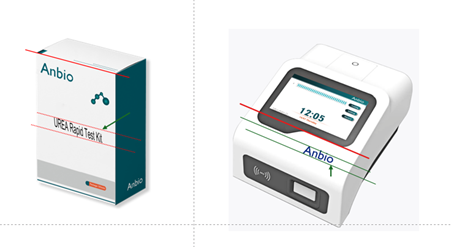

A timeline review shows that only a few months ago, Anbio’s website listed four devices and 62 test kits.

Between our initial check in early September and December 2025, the catalog expanded to around 450 products.

However, roughly 440 of these are test kits with identical packaging, differentiated only by a single line of text; often visibly and probably photoshopped. Many labels appear misaligned or inconsistent.

The product photos lack standard identifiers expected for medical devices:

- No lot numbers

- No manufacturing dates

- No importer or distributor details

- No CE or IVD compliance markings

- No unique packaging designs

This strongly suggests fabricated or non-existent product lines, created to simulate commercial activity. There may even be elements of counterfeit activism.

The R&D department does not appear anywhere on the website. No research process, no publications, no lab photos, no roadmap. The sales channel is likewise missing key information.

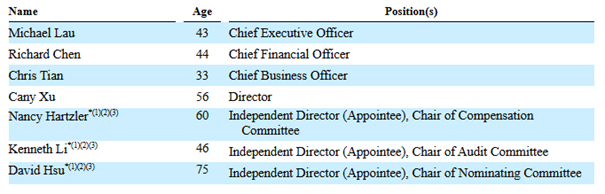

Management

Looking into management, the picture becomes clearer: Anbio does not merely lack a business model- it lacks corporate substance.

Identifying responsible individuals is especially difficult. The names disclosed in filings appear unusual:

- “Chris Tian” resembles a split form of the German name Christian.

- “Richard Chen” echoes “Richardchen”.

- “Michael Lau” phonetically overlaps with the feminine “Michaela”.

These anomalies may be coincidental, but given the overwhelming red flags, the pattern is notable.

Further issues: regulatory filings state that Michael Lau also serves as CEO of Genscript. Inquiries suggest he is unknown there. Genscript is a Nasdaq-listed Chinese company, which might initially suggest an overlap, but no connection could be confirmed. The commonality of the name complicates verification.

Given the risk of misidentification, we refrained from deeper forensic analysis of individuals.

For reference, the management team as disclosed to the SEC is shown below:

A closing reminder: the two main investor entities in the Cayman Islands (registered at the same mailbox address as Anbio itself) appear linked to James Howard (CVC, likely the convicted fraudster) and Mark Martinez (Northwestern Investment, with no traceable identity).

Financial Reporting

We did not scrutinize the financial reporting submitted during the listing application process, because:

- The financial statements for 2021–2024 are unaudited.

- They were prepared by the former CEO., and now-CFO, Richard Chen.

- Given the amount of obscurement and inaccurate information elsewhere, it is difficult to trust documents that are so easily compromised.

Structural complexity and documented anomalies elsewhere, leads us to not bother to rely on financial statements.