June 10, 2025

Summary

Douglas AG qualified as a subject for in-depth due diligence following its “stunning” performance post-IPO in March 2024, when the company managed to destroy over half of the raised capital within just six months. This prompted us to investigate the underlying reasons and to assess whether the worst is over – or if further losses are imminent.

Our research identified several unresolved issues, each pointing to serious structural weaknesses within the business. We highlight three critical problem areas:

- Misleading investor communication – Overly optimistic messaging during the IPO process now backfires as results fall short of forecasts and expectations.

- Unsustainable debt levels – Even after partial deleveraging with IPO proceeds, the remaining debt load appears too large, yet it is ignored by management.

- Outdated business model – Declining foot traffic in high-street locations combined with an online channel that is not meeting target clients’ specific needs are driving continuous customer attrition and yield falling sales numbers.

Even if Douglas could offset revenue decline by cutting administrative costs – a strategy that rarely succeeds – fixed interest costs cannot be changed except by paying back the debt. As a result, lower sales directly erodes profitability. Attempts to mask financial underperformance with “wokeness” and “DEI” will not appease disappointed investors. It will increase pressure to deliver short-term results, which is likely to hinder strategic reinvention, and thereby accelerating decline. There is no easy exit from this vicious cycle.

However, the most alarming finding emerged from what initially seemed a minor side task: reviewing Douglas’ corporate history. We quickly noticed glaring inconsistencies and omissions, particularly regarding the period from 1931 to 1969. The company’s official narrative omits nearly four decades – including the Nazi era in Germany– without explanation. This absence raised red flags and led us to investigate further.

What we discovered was deeply disturbing. Archival documents strongly suggest that:

- the Douglas Seifenfabrik likely used forced labor during the Nazi regime, and

- the Douglas perfumery may have been expropriated from its rightful owners under National Socialist rule and transferred to a Nazi businessman.

If even a fraction of this holds true, Douglas AG is sitting on a reputational time bomb. Legal and moral consequences are not theoretical. They are real, overdue, and no longer dormant.

Background

In 2013, the German merchant family Kreke held approximately 27% of public listed Douglas Holding AG. That same year, Müller Markt launched a hostile takeover attempt. To defend the family heritage, Henning and Jörn Kreke – then CEO and Chairman of Douglas – sought a strategic partnership with international investment firm Advent International. Together, they decided to acquire Douglas Holding AG themselves and delist it from the stock exchange including indices.

By this means the takeover attempt by Müller was successfully averted. Following the buyout by the Kreke family and Advent International, the retail conglomerate was broken up, and its assets – except the perfumery business – were stripped before the end of 2014. This marked the starting point of Douglas’s aggressive inorganic expansion strategy. The company acquired perfumery chains in France (Nocibé), in Spain (Bodybell, Perfumerías If), in Italy (Limoni, La Gardenia, Akzente), and in other European countries.

The efforts to streamline operations or cut costs proved more difficult than buying companies. On the contrary, it were acquisitions and integration complexity that led to a steady and troubling rise in debt. To regain control, a second IPO became inevitable in March 2024 – twelve years after Douglas had been taken private. The main objective was to use the IPO proceeds to repay a portion of the company’s mounting debt.

The IPO, however, turned out to be disappointing. It priced on the bottom of the marketed range at €25.30, then the stock dropped by 8.7% on its first trading day. Although the raised capital was used to repay part of the debt, it was not sufficient.

Today, Douglas shares trade at around €10 – reflecting a decline of roughly 60% within a year. Unsurprisingly, debt is once again on the rise.

We believe that a cacophonic corporate culture is often at the root of not only operational underperformance but also corporate malfeasance. In Douglas’s case, we were therefore unsurprised to find problems surfacing across various areas of business. While the company’s willful obfuscation of its Nazi-era heritage overshadows these issues, they are nonetheless worth highlighting.

Business Model and Financial Issues

Financial Reporting and Forecasting

In the fiscal year ending September 30, 2024 – just six months after Douglas’s IPO – the company’s market capitalization had been cut in half. In a display of remarkable detachment from operational reality, management responded not with strategic correction but with the launch of its laughable “Let It Bloom” campaign and a new, higher revenue target of €4.8 billion.

But reality hit fast. When Q1 (FY) results were reported, Douglas missed profit expectations dramatically. The company subsequently backtracked on its IPO promise to pay a dividend. Revenue guidance was quietly revised downward to €4.5 billion – a 6% cut in just one quarter. Projected linearly, this implies a full-year 2025 revenue of just €3.7 billion – a staggering 22% shortfall versus original expectations.

Douglas blamed “slowing demand.” Slowing demand? They claim to be surprised by market deterioration – just months after projecting aggressive growth? Either management lied then, or they are incompetent now.

Likely both. The contrast between the strong growth narrative pre-IPO and the immediate downturn post-IPO suggests management was aware of underlying issues. Consider the following:

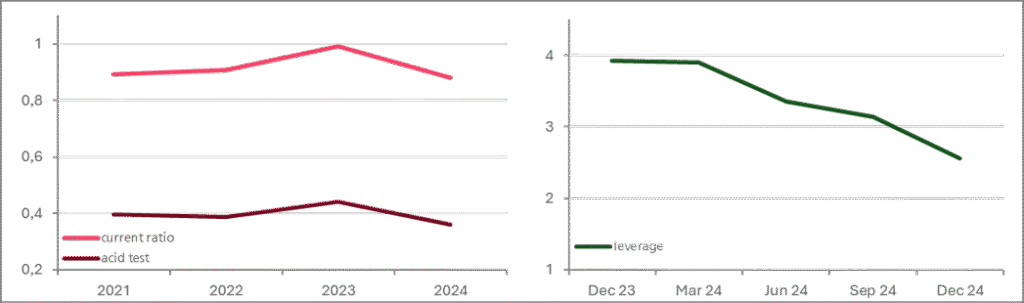

Leverage Ratio: Douglas AG proudly communicated a reduction in its (quarterly) leverage ratio from 4.0 (as of December 31, 2023) to approximately 2.3 by December 31, 2024 – Q1 of its fiscal year. But this reduction was purely the result of debt repayment using IPO proceeds. A comparison with full year numbers is not even possible since negative Equity leads to a meaningless Leverage ratio (of -18.5).

Interest Expense: Management claimed that refinancing under better terms would reduce interest expenses by up to €100 million annually. Yet the FY 2024 report shows an annual saving of just €30 million. More troubling: quarterly interest payments are €35 million higher than in the corresponding quarter of 2023.

Sales Performance: Pre-IPO revenue growth of 11.5% has dropped to 5.8% as of December 31, 2024. Meanwhile, cost of sales rose to 7.8% over the same period. The performance of Douglas’s online segment could not be independently verified.

Even though pre-IPO financials were audited, audits at this stage face significantly less regulatory scrutiny than those of listed companies. The use of broader accounting practices is permitted. What can be ruled out is any market-driven pivot in Douglas’s financial trajectory – there was no bigger macroeconomic regime shift in 2023 or 2024. Instead, the suspicion arises that overly optimistic figures were presented in the run-up to the IPO to attract investors and secure a higher valuation.

Troubling Debt Level

IPO capital was used to reduce long-term debt from €3.4 billion to €2.1 billion, thereby lowering the total debt burden from €3.7 billion to €2.4 billion. Current liabilities remained unchanged. While this move may appear prudent on the surface, it has failed to reverse Douglas’ deteriorating financial health.

Because Douglas’ inventory is difficult to liquidate quickly, we looked at the current ratio and quick ratio as indicators of financial resilience. Alarmingly, both ratios have consistently remained below critical thresholds (1.0 for current ratio, 0.5 for quick ratio), and fall even further below retail industry averages (1.4 and 0.7, respectively). Hitting all-time lows just six months post-IPO is particularly concerning – either management is unable to arrest the decline or unwilling to do so.

The explanation for this lies in how Douglas’ management traditionally governs: With its eye on the leverage ratio, calculated by using total (not short-term) debt. That ratio, shown quarterly in the figure, appears to trend in the right direction. But, as previously discussed, it is fundamentally flawed due to negative equity prior to the IPO. This offers a textbook case of how reliance on misleading KPIs can endanger a firm – even when “targets” are formally met.

Branches in Decline

With most branches in shopping malls and high-street locations, Douglas is directly impacted by collapsing foot traffic. Demographics, policy, and security fears all play a role: an aging society, car-restricted city centers, and a public increasingly uneasy about visiting urban centers.

At the same time, the core of Douglas’s business – luxury fragrance – is now widely available in drugstores like i.e. Müller, often at lower prices. Consumers have shifted. Douglas has not. The result is ongoing customer attrition.

Online Business: Out of Touch

Douglas does maintain an e-commerce presence – but who buys fragrance online?

Those who already know what they want can purchase it cheaper on Amazon. Those seeking discovery or gifting still need to test scents in person.

Douglas has failed to acknowledge this fundamental consumer truth. Its digital strategy is neither differentiated nor suited to a product category that is inherently experiential. What remains is underperformance, veiled in a tech-savvy facade.

Wokeism

Douglas is one of the last German corporations clinging to wokeism, proud but misaligned with global consumer sentiment. While competitors shift toward value and meritocracy, Douglas signals virtue in a language that no longer – if it ever has – converts to revenue.

Directors’ Dealings

Douglas holds the record in Germany for director’s dealings – ogging up to 80 per year. Management seems to spend more time on their trading than the company strategy. This isn’t stewardship. It’s pure value extraction.

Corporate History Issues

Douglas remains conspicuously silent about its history between 1936 and 1969. The website shows a strange omission, particularly in a country where corporate accountability for the Nazi era is expected. While many companies have taken steps to address their past, Douglas appears to have deliberately avoided doing so. When we dug slightly deeper, we could hardly believe the indications we found.

The Douglas ‘Seifenfabrik’

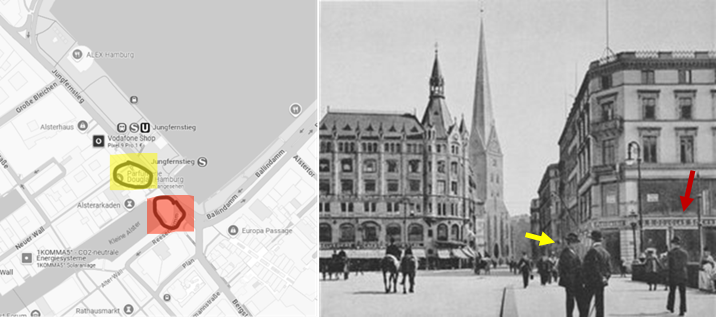

The official corporate history begins in 1820 with the founding of the Douglas Seifenfabrik. The founder’s sons eventually took over and grew the manufacturing firm. Many years later, it was led by Mrs. Kolbe, who licensed the name “Douglas” to the Carstens sisters in 1910. The Carstens sisters then opened a perfumery on Hamburg’s high street Neuer Wall to sell Douglas products – though not exclusively.

Largely unknown is the fact that the Seifenfabrik had operated its own perfumery from 1890 to 1908 – at almost the exact location where the Carstens sisters opened theirs in 1910. The circumstances under which the Seifenfabrik closed its store while simultaneously licensing the name to a new shop just 50 feet away remain unclear.

blue: Douglas & Sons till 1908, green: Perfumery Douglas by Carstens sisters from 1910

Despite the brand connection, the factory and the perfumery remained separate legal entities until 1998. It was not before 1998, when Douglas Perfumery acquired the Seifenfabrik, probably to end the licensing agreement and to gain full legal ownership of the brand.

It was Mrs. Kolbe who recommended Mr. Erhard Hunger – someone personally known to her – to the Harders family. Hunger was to be appointed as an authorized signatory for the perfumery in 1936. However, Mr. Hunger would later turn out to have played a decisive, and potentially sinister, role during the Nazi era. Whether Mrs. Kolbe recommended him in good faith remains unclear.

There are only a few official records available on the Seifenfabrik after 1936. Some of them are in our possession, and they suggest that the Seifenfabrik could have used forced labor during the Nazi regime.

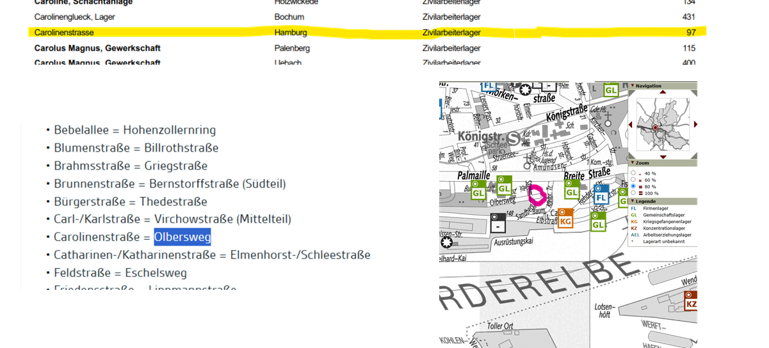

Circumstantial evidence comes from an official German list of approximately 2,500 companies known to have used forced labor. In cases where companies could not be identified directly, only the address where forced labor was deployed is listed.

Though there are documents that the sons of Scottish founder John Sharp Douglas moved their production to a larger facility outside of Hamburg at about 1847. But they kept Carolinenstrasse as their office location. For some reason Douglas’ office address has been redacted, maybe just to obfuscate forced labor usage.

Headquarter address redacted (probably Carolinenstrasse 3, Hamburg)

The Douglas Perfumery

The perfumery that would later become today’s Douglas corporation was founded in 1910, when the Carstens sisters were granted a license to use the Douglas name by Mrs. Kolbe of the Douglas Seifenfabrik.

In 1929, the business was inherited by the Harders family and officially renamed Douglas Harders & Co. in 1931. This is where Douglas’ official history begins to diverge from the documented facts.

In response to our inquiry, Douglas confirmed that Mr. Erhard Hunger, by recommendation of Mrs. Kolbe, was appointed by the Harders family as an authorized signatory in 1936. When Mr. Hunger was drafted into military service in 1939, a Mr. Poss allegedly took over his role.

Douglas also claims that Hunger’s appointment was mandated by the Dritte Verordnung über den Aufbau des deutschen Handwerks (Third Ordinance on the Structure of German Crafts) from 1936, which required all firms in Nazi-Germany to appoint a certified manager. Furthermore, Douglas states that Ms. Eugenie Schalt, the first employee hired by the Carstens sisters, had been informally managing the business on behalf of the Harders family since 1931.

(Third Ordinance on the Structure of German Crafts)

Douglas claims the perfumery was closed in 1943 due to WWII and allegedly reopened by Ms. Eugenie Schalt. Supposedly this happened in coordination with Mr. Hunger, who was in a Canadian prisoner-of-war camp until 1947. According to Douglas’ corporate history, Mr. Hunger managed the firm as sole owner from 1945 to 1969.

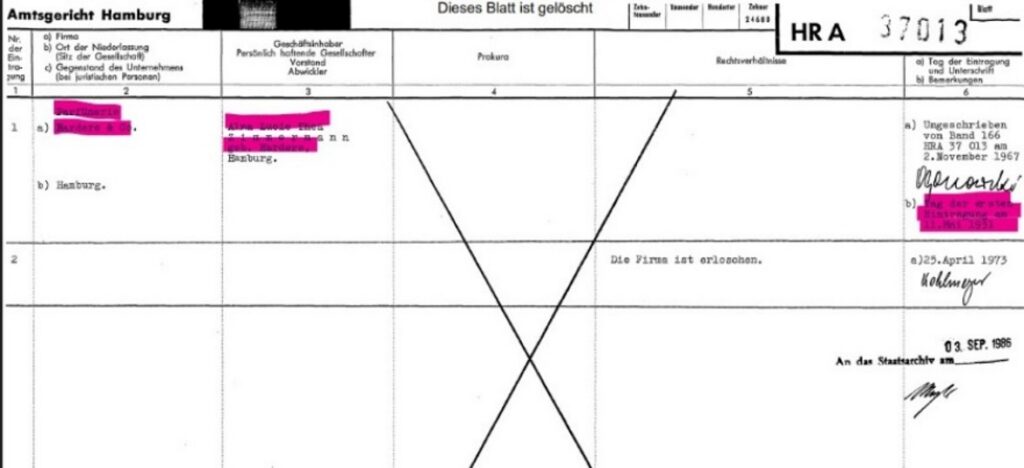

This narrative is riddled with contradictions and demonstrable inaccuracies. Our research in official German archives confirms that Douglas Harders & Co. remained active until at least 1973 and was legally owned by Mrs. Alma Lucie Thea Zimmermann (née Harders). This record shows that the company inherited and operated by the Harders family was different from the entity that evolved into today’s Douglas brand.

Douglas itself states that the perfumery was owned by Hertha, Lucie, and their father Johannes Harders. Notably, Lucie’s actual first name is Alma, a name of Hebrew origin. Is Douglas concealing the Harders family’s possible Jewish heritage?

Aside from the registry entry, we were unable to find any further traces of the Harders family.

Last owner: Alma Lucie Thea Zimmermann née Harders

When put together, a much clearer and darker picture emerges. The evidence strongly suggests that the Nazi regime stripped the rightful owners of their business and transferred it to Mr. Erhard Hunger in 1936. This was a common mechanism the Nazis used to gradually expropriate Jewish and other “non-Aryan” business owners.

This theory also explains how Mr. Hunger returned from the PoW camp in 1947 and took over as sole owner of the perfumery. Clearly he held a position that had no clear legal or economic basis unless one assumes expropriation.

Douglas’ current historical narrative, however, makes little sense. According to it

- Mrs. Kolbe recommended her friend Mr. Erhard Hunger to the Harders family,

- Ms. Eugenie Schalt, a long-time acquaintance of the Carstens sisters, managed the shop informally for the Harders family,

- the perfumery was reopened by Ms. Schalt on behalf of Mr. Hunger – while Mr. Hunger was still a PoW in Canada, and yet

- no details are provided about how ownership passed from the Harders family to Mr. Hunger.

It doesn’t add up. The theory that best explains these contradictions, and unfortunately the one most consistent with historical patterns of Nazi-era expropriation, is also the most uncomfortable and regrettable one to face.

One final piece of evidence further reinforces this view: In 1953, Mr. Erhard Hunger founded a new legal entity called Parfümerie Douglas GmbH (LLC).

In 1969, Douglas GmbH, which by then included six Douglas perfumeries across Hamburg, was sold by Erhard Hunger to Hussel AG. It appears likely that Mr. Hunger founded the GmbH to repackage what he had acquired, very possibly through Nazi-facilitated expropriation, into a more legitimate-looking corporate vehicle. This allowed him to sell the business without being asked difficult questions about its true origins.