We have already reported on the questionable governance practices at HelloFresh, particularly concerning the founders and CEO/COO duo, Dominik Richter (DR) and Thomas Griesel (TG). Over the past years, the company has not only tolerated but seemingly normalized behavior that should raise concerns among shareholders.

One striking example is the adjustment of bonus-relevant objectives within the fiscal year – effectively moving the goalposts for management compensation. Meanwhile, TG and DR have engaged in such an extraordinary volume of directors’ dealings that HelloFresh consistently ranks among the German companies with the most insider transactions. Beyond their official duties, both established private investment vehicles – TGS Ventures and DSR Ventures – a substantial distraction from their core management responsibilities.

The governance concerns do not end there. It surfaced that Richter served as CEO of Tio Tech SPAC between 2021 and 2023 (liquidation). However, the supervisory board, instead of scrutinizing the conflict of interest, approved the arrangement in retrospect and declared that no negative impact was expected.

Richter’s Trades: The Role of Share Pledging

A closer look at Richter’s reported transactions reveals a clear pattern. Most are not straightforward sales or purchases of HelloFresh stock but pledges of shares. On a few occasions, filings indicate “acquisitions”, but these are not open-market purchases. Rather, those transactions are linked to pledge agreements, often in reaction to margin calls.

The purpose of pledging is simple: t allows an executive to unlock liquidity from their holdings without selling them. By pledging shares as collateral, directors can obtain loans while formally retaining stock positions and voting rights. This avoids the reputational scrutiny that would come with outright disposals, especially if a director sells his own stock

How Pledging Works

A pledge arrangement is typically governed by a private agreement between the director and a bank, resembling a swap structure:

- The director pledges shares to the bank.

- The bank provides a loan against the pledged collateral.

- Initially, the director retains voting rights.

Once the shares are pledged, two settlement paths are possible:

- If the share price rises: -the collateral becomes excessive. The bank may purchase the excess shares from the director, transferring voting rights to the bank.

- If the share price falls: collateral becomes insufficient, triggering a margin call. The director may then acquire additional shares from the bank. Those are either newly bought or transferred from the bank’s holdings. In this case, voting rights shift to the director.

Regulators permit pledging on the grounds that directors remain incentivized to support rising share prices. They even tolerate that pledged shares may be sold if prices rise and collateral requirements decrease.

However, many corporations have recognized the risks and introduced internal restrictions on share pledging by directors. Unsurprisingly, HelloFresh is not among them.

Why It’s a Problem

Research and empirical evidence point to several structural issues with share pledging:

- Short-term bias: Directors focus excessively on short-term price stability to avoid collateral calls, at the expense of long-term strategic decisions.

- Loss of focus: Pledged executives tend to devote less attention to the core business model, with incentives skewed by personal liquidity needs.

- Financialization: Companies where pledging is common often resort to financial engineering, including share buybacks, to stabilize prices.

- Debt misalignment: Directors may perceive themselves as doubly indebted – through personal loans and corporate debt, thus leading to distorted decision-making.

- Volatility: Studies show that pledging correlates with higher stock price volatility, harming ordinary shareholders.

In sum, pledging creates a fundamental conflict of interest between directors and shareholders.

The DSR Case

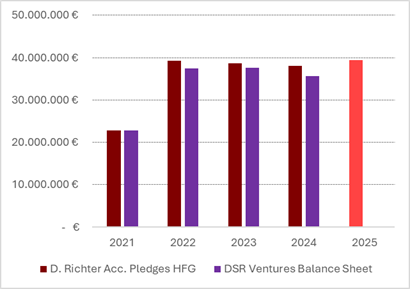

We examined Richter’s pledging activity at HelloFresh. He began significant pledging in 2021 and has since pledged 6,645,000 shares, with an aggregated pledge value of approximately €108m at the time of transaction.

The bank involved is most likely Morgan Stanley, based on voting-rights notifications. Over four years, 178 notifications were issued reflecting changes in Morgan Stanley’s voting rights in HelloFresh. This is roughly ten times more than the next reporting institution.

The loans appear to have been largely used to fund Richter’s vehicle DSR Ventures. But the declining HelloFresh share price has eroded collateral value: The initial €108m loan base has shrunk to around €40m. Several times, additional shares had to be purchased by DSR Ventures to cover margin calls.

For example, most recently following the Q2 2025 results, HelloFresh shares fell 15%, triggering a margin call. DSR Ventures then acquired 4.8m shares from its banking partner to restore collateral.

The following table we have consolidated the pledge transactions and their associated loan values of DSR ventures (latest margin call after Q2 2025 reporting not included).

| Date | Type | Shares | Price | Acqusisition | Loan | Cum. Load |

|---|---|---|---|---|---|---|

| 17.03.2025 | Pledge | 500.000 | 8,454€ | 4.227.000€ | 39.362.580€ | |

| 17.03.2025 | Acquisition | -500.000 | 8,267€ | 4,133.250€ | ||

| 07.02.2025 | Pledge | 500.000 | 11,894€ | 5.947.000€ | 55.247.630€ | |

| 30.09.2024 | Pledge | 660.000 | 9,196€ | 6.069.360€ | 38.117.420€ | |

| 06.09.2024 | Pledge | 1.500.000 | 6,732€ | 10.098.000€ | 23.494.020€ | |

| 06.09.2024 | Acquisition | -1.500.000 | 6,710€ | 10,065.000€ | ||

| 15.08.2024 | Pledge | 1.000.000 | 6,306€ | 6.306.000€ | 21.976.410€ | |

| 02.02.2023 | Pledge | 610.000 | 12,150€ | 7.411.500€ | 30.192.750€ | |

| 21.12.2022 | Pledge | 550.000 | 20,970€ | 11.533.500€ | 39.318.750€ | |

| 09.09.2022 | Pledge | 300.000 | 25,230€ | 7.569.000€ | 33.429.750€ | |

| 02.09.2022 | Pledge | 300.000 | 26,440€ | 7.932.000€ | 27.101.000€ | |

| 27.05.2022 | Pledge | 250.000 | 34,230€ | 8.557.500€ | 24.816.750€ | |

| 04.03.2022 | Pledge | 200.000 | 49,720€ | 9.944.000€ | 23.617.000€ | |

| 30.06.2021 | Pledge | 275.000 | 82,780€ | 22.764.500€ | 22.764.500€ |

Contrasting the cumulative loan values with the balance sheet of DSR Ventures suggests that the borrowed funds have been channeled into its operations and investments.

Conclusion

Dominik Richter’s behavior demonstrates a persistent distraction from his responsibilities at HelloFresh. His external commitments (including the SPAC engagement and the build-up of DSR Ventures) already cast serious doubt on his ability to act as a fully dedicated CEO. The extensive pledging of shares further amplifies these concerns, particularly since the borrowed funds appear to be channeled into illiquid and high-risk ventures.

The consequences are already visible. This year, HelloFresh expanded its share buyback program from €70m to €100m. Another move that raises legitimate questions as to whether capital allocation serves the company and its shareholders, or whether it primarily stabilizes collateral values for pledged shares.

The pattern is unmistakable: DSR Ventures has become the true focus of Richter’s activities, while HelloFresh increasingly functions as a financing vehicle. Such a setup runs directly against the interests of shareholders, who are effectively paying for Mr. Richter’s private business matters while additionally carrying the risk.

We therefore demand that Mr. Richter step down from his role at HelloFresh SE, or, failing this, that the Supervisory Board act in its fiduciary duty and dismiss him. Anything less would constitute a clear breach of responsibility towards shareholders.

Even if the Supervisory Board acts decisively (which we do not expect), by replacing Dominik Richter and forcing a fundamental change of governance, the immediate effect will not be positive for the share price. Such a move would amount to an admission that mismanagement and conflicts of interest have been tolerated for years. Markets are unlikely to ignore this. In the short term, investors should expect a sharp correction as the scale of the problems becomes undeniable.