We are short HelloFresh SE (HFG, Xetra), the world’s largest provider of meal kits and ready-to-eat meals for home preparation. We see a variety of interconnected problems, which it is now too late to resolve in isolation.

Summary

Falling Customer and Order Numbers

Since 2022, the number of active customers and orders has been steadily declining. Revenue stability was achieved due to price increases, utilizing global inflation. However, such a strategy has its limits, and the recent reduction in customer numbers has reached a level where the company no longer publicly discloses this key metric.

Earnings Decline in 2024

After years of rising profits, HelloFresh is expected to post a significant loss in 2024. Rising procurement, logistics, and marketing expenditures are primarily responsible for this downturn. Notably, these costs have increased from 91.6% of revenue in 2023 to 96.1% in 2024.

North America Prophecy

In north America revenue from ready-to-eat product has compensated for revenue decline of cooking boxes. Still, North America has suffered a massive decline in profitability. From a profit of €89 million in the first half of 2023, the North American segment has plunged to a loss of €60 million in 2024. It’s a question of time until these trends manifest themselves in Europe, too. However, in Europe, HelloFresh has no RTE offering that could compensate for decline in its core business.

Management’s Lack of Experience

The two co-founders, Dominik Richter and Thomas Griesel, have led the company since its inception. However, their management style has proven insufficient in navigating the company through its current phase of decline.

Aggressive and Questionable Marketing Tactics

HelloFresh’s aggressive marketing approach has also raised red flags. The company has been fined in the UK for repeatedly contacting former customers who had explicitly requested not to be contacted. This has led to reputational damage in several key markets.

ESG Violations and “Greenwashing” Accusations

HelloFresh has been involved in several controversies related to its ESG commitments. From false claims about the sourcing of meat in Spain to accusations of supporting animal cruelty in Thailand, the company’s actions have contradicted its sustainability promises. Moreover, HelloFresh was found guilty in a German court for misleading consumers about its carbon neutrality.

Management’s Focus on Personal Financial Gains

Both co-CEOs have engaged in a significant amount of personal financial transactions involving HelloFresh shares, creating conflicts of interest. These transactions, conducted through their respective venture capital firms, raise concerns about their commitment to the company during this critical period.

Board of Directors’ Lack of Oversight

The board is largely composed of individuals with ties to private equity firms, which may not have the long-term interests of the company in mind. This further reduces the likelihood of corrective action being taken at the executive level.

Background/History

HelloFresh’s business model revolves around assembling ingredients for meals in meal kits, delivered to customers through subscriptions. Customers then prepare the meals themselves using illustrated recipe cards, which can take up to 30 minutes, though this saves time shopping for groceries. Around 50 recipes rotate weekly for customers to choose from. Ready-to-eat meals were later introduced in Australia and the U.S. These meals only need two minutes in the microwave but have the charm of an in-flight meal on a long-haul flight.

The meal kit business idea was the foundation of HelloFresh, launched by Dominik Richter, Thomas Griesel, and Jessica Nilsson, all in their early 30s, in November 2011 in Berlin. Venture capital firm Rocket Internet liked the concept and contributed €3.7 million in the first funding round. By 2014, additional rounds of financing raised about €150 million for the young company. In 2017, HelloFresh went public with a valuation of around €1.7 billion as one of Germany’s rare unicorns.

Growth and Overreach

However, investors demanded the promised, reckless growth, forcing the young founders into increasingly unconsidered action, for example:

- Even before its business in Germany took off, HelloFresh expanded to the Netherlands, the U.S., the U.K., and Australia within its first year in 2011.

- In 2016, HelloFresh attempted to attract subscribers for wine selections (around €15 per bottle), only to abandon the effort a year later.

- In March 2018, HelloFresh acquired the U.S. company “Green Chef” to expand its recipe offerings, including vegan options.

- In October 2018, HelloFresh Canada took over meal kit company “Chefs Plate.”

- 2018 also saw the launch of “Every Plate,” a discount brand for the U.S. market.

- In 2020, HelloFresh purchased U.S. company “Factor75” (Factor) for $277 million. Factor offers fresh, pre-cooked meals that, unlike meal kits, only need reheating in a microwave.

- In 2021, HelloFresh acquired Australian company “youfoodz,” which offers ready-to-eat meals like Factor.

- In April 2022, HelloFresh expanded to Japan but had to withdraw within half a year due to insufficient returns.

- In August 2023, HelloFresh began reverse-expanding Factor to Europe, starting in the Netherlands.

- In 2024, HelloFresh acquired American online butcher “Good Chops.”

- Also in 2024, HelloFresh entered the U.S. pet food subscription market with “Pets Table.”

However, as one initiative followed the other, acquired companies remained unintegrated und continue to operate under their old brands. In some cases, they compete against other HelloFresh brands. The organizational structures of the acquired companies have also seen little adjustment. Additionally, the launch of new HelloFresh brands, such as Every Plate, further complicates the structure and processes.

The sprawling structure makes managing HelloFresh as a group highly inefficient. The business has become regionally and product-wise unmanageable, resembling a conglomerate, but without the necessary tools, processes, or competencies to run one.

Profitability and Sustainability

We began closely examining HelloFresh due to vague uncertainties regarding the sustainability of its business model:

- The pandemic significantly boosted HelloFresh’s business. People, fearful and stuck at home during lockdowns, found it convenient to “shop” safely and prepare quality meals. However, these habits have not become the “new normal,” as many predicted or hoped. Consequently, customer numbers and orders began to decline in 2022.

- The market potential for further growth remains questionable. Not everyone enjoys the concept of meal kits. Urban singles might prefer spending €12.50 on a quick meal, like a kebab, rather than cooking for themselves. Similarly, older generations, who have shopped and cooked all their lives, might not be enthusiastic about cooking from unfamiliar recipes. Many working professionals might also be reluctant to commit to subscriptions and miss out on spontaneous dinner plans or drinks with colleagues.

- The competition is increasing, with companies like “etepetete” in Germany or “Blue Apron” in the U.S. successfully poaching HelloFresh customers.

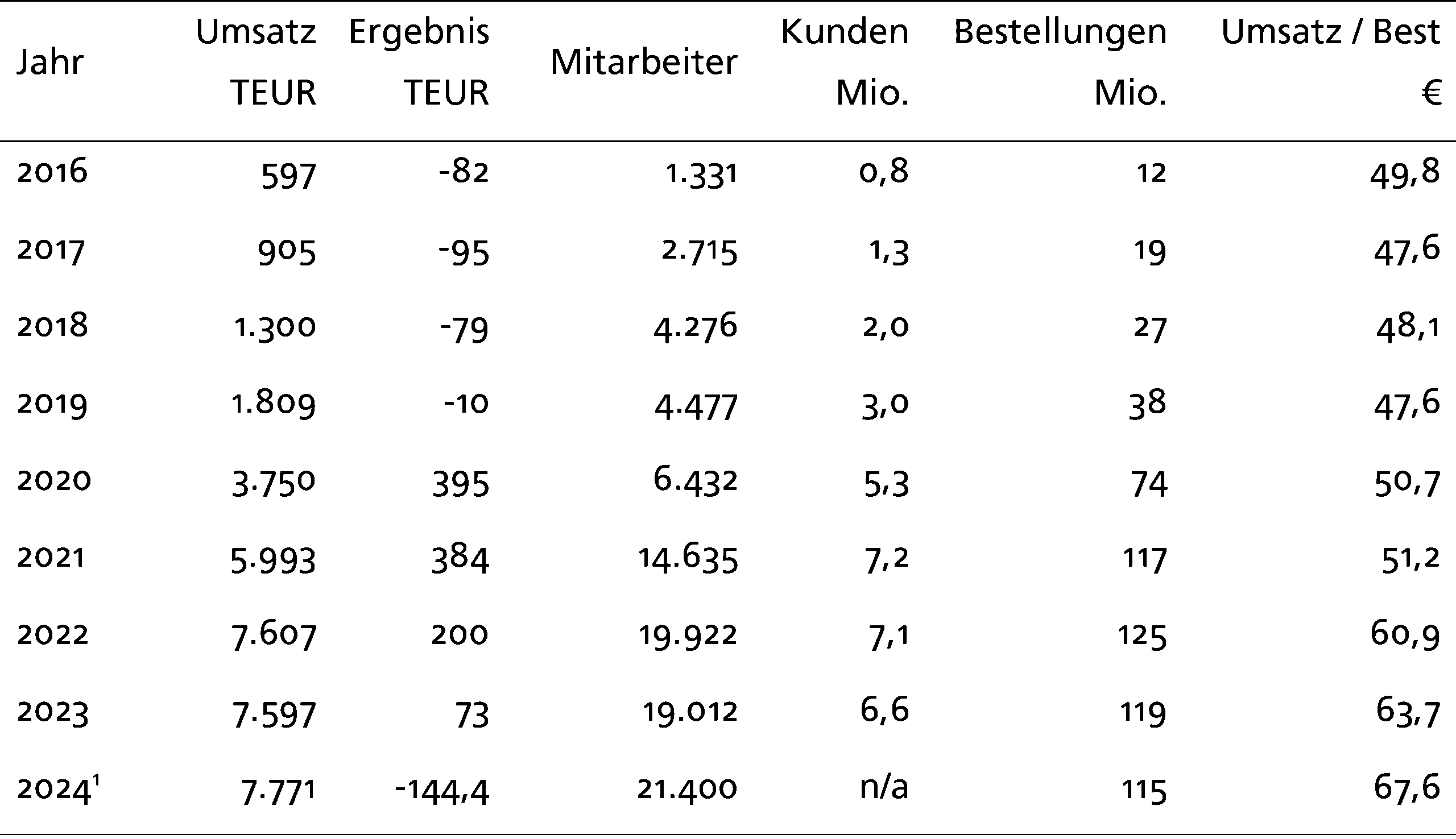

The following table shows the development of HelloFresh’s key financial figures since a year before its IPO, i.e., since 2016:

By 2022, as the pandemic began to subside and global measures were lifted, HelloFresh’s orders and customer numbers started to decline. In fact, the number of active customers had always been mentioned on the second page of each half-year and quarterly report. However, it has been absent since the Q1 2024 report, possibly indicating that the scale of customer loss has become so significant that the company no longer wishes to highlight this figure prominently.

A closer look at the key figures shows that despite the declining number of orders and customers since 2022, revenues have continued to rise. This is reflected in the average order value. The overcompensation for fewer orders by fewer customers can likely be attributed to price increases, which have also occurred at HelloFresh in the face of global inflation. For example, in Germany, a meal kit for two people and two meals per week (four dishes) cost €35.49 in 2022. In 2023, the price increased by 11% to €39.49, and by 2024 it rose again by 2.5% to €40.49. While it’s difficult to generalize the German example to the entire world, the increase in average order value, at 11.1%, is strikingly similar.

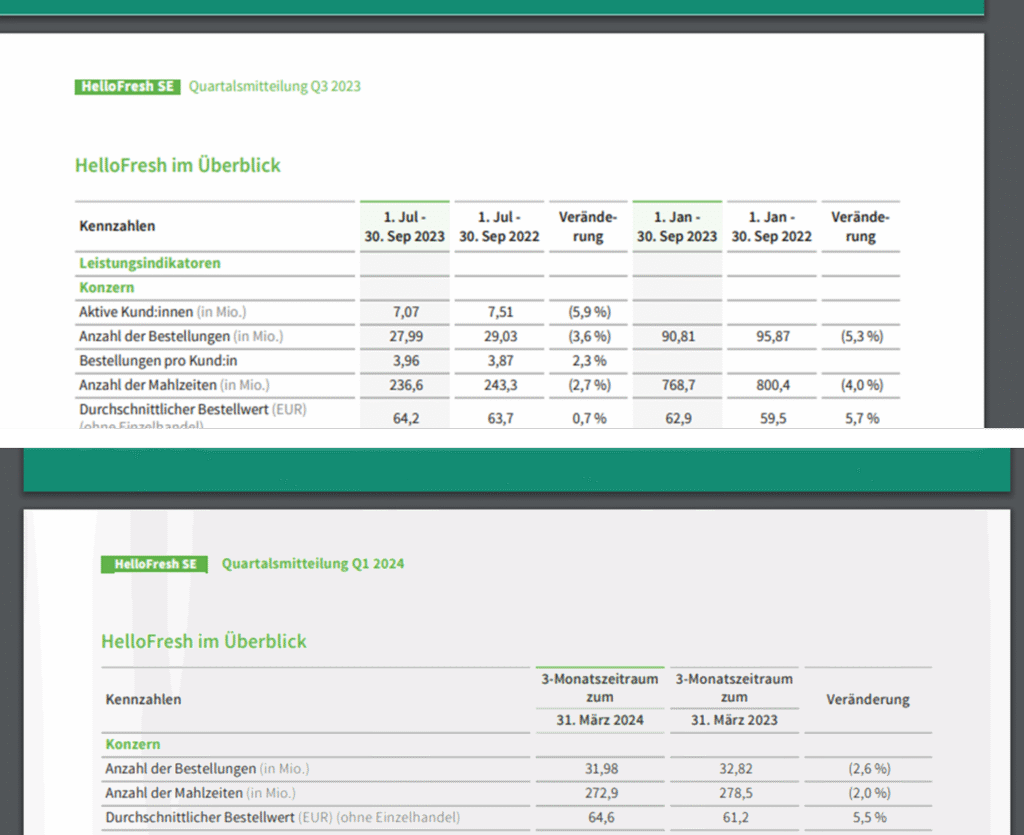

We have estimated the 2024 results based on previous years’ experiences and the results from the first half of 2024. The half-year report for H1 2024 shows a loss of €75 million. This loss did not result from special effects but from significantly increased procurement, logistics, and marketing costs. While these costs accounted for about 91.6% of revenue in 2023, they rose to 96.1% in 2024. For this reason, we find it justified to extrapolate the result from H1 2024 to the full year. We do not believe that the current management can adequately control the costs, leading to an estimated annual loss of €144 million for 2024.

According to segment reporting, as in previous years, about two-thirds of HelloFresh’s revenue comes from North America, and one-third from the “International” segment, which includes everything outside the US and Canada. The report also shows that the result in North America has declined by €140 million compared to H1 2023, dropping from €890 million to -€60 million. The international segment contributed a small margin with an EBIT of €6 million. The loss, therefore, occurs despite the compensation in North America.

Around three-quarters of HelloFresh’s business is based on its high-margin meal kits, while about one-quarter comes from its lower-margin ready-to-eat business. In the US (where HelloFresh primarily offers ready-to-eat meals), the 9% revenue loss in meal kits has been offset by a 50% increase in ready-to-eat meal revenue. Therefore, the international segment, which cannot be subsidized by ready-to-eat meals, likely experiences smaller declines in meal kits. However, trends from the US often arrive in Europe with a delay. We do not believe that HelloFresh has enough time to introduce ready-to-eat meals in many countries in the international segment.

Management

It is unusual that the two founders, Dominik Richter and Thomas Griesel, have been leading the company as co-CEOs since its inception. Different leadership skills are needed at various growth stages, which few managers possess. We do not believe that the current board is capable of achieving the turnaround that is now required.

The board’s lack of experience and competence has already manifested itself in culturally inappropriate behavior towards employees. After serious accusations of poor working conditions in the US business, the conflict between the founders and American syndicates escalated to the point where workers resigned en masse or even sabotaged deliveries. As the quality of the boxes declined, customers followed suit.

Despite legal disputes with unions over blocking the introduction of employee representation, similar issues occurred in Spain and Germany. In Japan, HelloFresh was convicted for not adhering to minimum notice periods after closing its business.

HelloFresh’s aggressive marketing is also noteworthy. In all regions, former customers have complained about being repeatedly contacted by the company via phone, even after explicitly stating that they did not wish to be contacted. This led to a £140,000 fine in the UK after the data protection authority demonstrated that HelloFresh had sent millions of emails to former customers and continued to contact them by phone even after requests to stop.

Additionally, several breaches of ESG (Environmental, Social, and Governance) guidelines have come to light.

When HelloFresh began its operations in Spain, activists quickly revealed that the company’s promise to use “100% Spanish-raised beef, chicken, and pork” was false. At the same time, HelloFresh was forced to halt the import of coconut milk from Thailand after PETA accused the company of being aware for some time that monkeys were being used as slave labor to harvest the coconuts.

In these disputes, there is a lingering accusation that the company is engaging in “greenwashing.” Later, the German environmental organization Deutsche Umwelthilfe sued HelloFresh for its claim of being carbon-neutral and won the case in the Berlin Regional Court.

In all these cases, at least one of the two CEOs, Dominik Richter or Thomas Griesel, was personally involved. Notably, these incidents became more frequent after the core investors, Rocket Internet and Vorwerk, sold their combined nearly 50% stake in the company. From a shareholder perspective, it is unacceptable that the inexperience and cultural insensitivity of the management team repeatedly lead to extraordinary costs and endanger the investment.

The Board of Directors offers little corrective action.

Three of the four current board members, including the chairperson and the vice-chair, are also employed by private equity firms and were likely appointed to the board as a condition of HelloFresh’s investment. Even if alarm bells are ringing within the board, the public is unlikely to hear about the problems until these members have secured their own interests.

Side Businesses

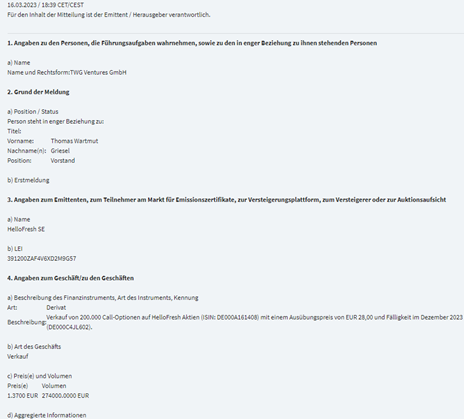

The regulatory disclosures of insider trading by HelloFresh executives are shocking. The two CEOs are exceptionally active when it comes to trading HelloFresh shares and derivatives, often appearing in 5-10 reportable transactions per year, either personally or through their venture capital companies, TWG Ventures (for Thomas Wartmut Griesel) and DSR Ventures (for Dominik Sebastian Richter).

These venture companies were founded and have been operational for years, so the question arises: why did they only begin reporting transactions under the companies’ names since August 2024, when they had previously reported them under their own names?

But this is just a side note, as the transactions themselves are far more concerning. Dominik Richter frequently pledges his HelloFresh shares outside of a trading system as part of credit transactions. The shares are typically purchased shortly before. This method obscures the purpose and result of the transaction, as the transfer of shares to the creditor, the return of shares to the borrower, or the sale of shares by the creditor are not subject to reporting requirements. The volume of these transactions regularly involves 1-2 million shares, which at the current share price amounts to between €10 million and €25 million. This occurs four to six times a year.

Thomas Griesel acts similarly, although more frequently, and also does not use a public trading system for his transactions. However, he engages in different types of securities transactions. In most cases, he sells near-money put options on HelloFresh for approximately 1-2 million shares, earning a premium of about half a million euros. These transactions become transparent when the counterparty exercises the options and Griesel must settle the transaction. More concerning are his occasional sales of call options on HelloFresh shares, which create a direct conflict of interest with his role as CEO.

In any case, it is generally not in the interest of HelloFresh shareholders for both co-CEOs to be more occupied with their private financial transactions and venture capital businesses in the midst of a corporate crisis than with managing the struggling company.

Conclusion

HelloFresh has reached a critical juncture. Its core business model is under pressure, and the management team has shown an inability to adapt to the current challenges. The company’s dependence on price increases to offset falling customer numbers is not sustainable in the long run. Meanwhile, labor disputes, management controversies, and reputational damage are piling up.

The stock price of HelloFresh is still driven by the belief of some investors in a young, miracle start-up, a phenomenon reminiscent of the hype surrounding Wirecard. Some may recall that HelloFresh was briefly included in the DAX, from September 2021, when the DAX expanded from 30 to 40 companies, until September 2022. During that time, HelloFresh shares lost 70% of their value.

Some of the issues described here have already been reflected in the share price. For instance, following the release of the last annual report in March 2023, the stock fell from €12.04 to €6.66, losing 45% of its value. The stock hit its lowest point at €4.12 in July. Since then, HelloFresh has recovered approx.. 8-9€.

We strongly believe that HelloFresh’s stock is significantly overvalued at its current price. Our target price of €2.50 reflects a realistic assessment of the company’s prospects, meaning we expect a decline of at least 70% from the current level.